With Vietnam being identified as a regional outperformer for exports, local businesses should remain alert to export credit risk and take steps to protect their cash flows.

Vietnam is one of the fastest growing ASEAN economies. It has been identified by economists as one of the world’s most promising markets for growth and investment, with GDP predictions for 2021 indicating growth of at least 7%. According to the Atradius report Promising Markets for 2021, Vietnam is one of a handful of countries providing opportunities for investors and exporters. It is also one of just a small number of countries throughout the world that successfully avoided recession during 2020 and is recognised as a regional outperformer for exports.

According to the United Nations COMTRADE database on international trade, almost half of Vietnam’s exports are directed towards Asia (49%), with the greatest proportion of exports going to China, Japan and South Korea. However, on a country-by-country basis by far the greatest percentage of Vietnam’s exports heads to the US. This amounts to 28% of all of Vietnam’s exports, followed by China (including Hong Kong) at 21.8% and then Japan and South Korea both receiving 7% of Vietnam’s exports.

With such a significant proportion of Vietnam’s trade exports heading to just two markets, Vietnam’s businesses could benefit from paying close attention to the B2B payment behaviours in both countries. To survive and thrive in a global market, Vietnam’s businesses need the security of solvent, reliable customers that pay on time, underpinned by robust credit management policies and practices.

What are the payments behaviours of Vietnam’s primary markets: US and China?

Every year Atradius monitors payments behaviours in key sectors and markets throughout the world. The Payments Practices Barometer Survey assesses key benchmarks such as the percentage of credit offered in a sector and market, average payment terms, DSO (Days Sales Outstanding) and the percentage of sales that are written off.

The results of this year’s Atradius Payments Practices Barometer Survey for the US are concerning. Nearly half of the businesses in Vietnam’s primary export destination reported deterioration in the payment practices of their customers. 50% of B2B invoices were paid late and 8% were written off, far more than reported by their regional peers. This is substantially fewer than the 50% of businesses that plan to absorb any bad debts internally (an inherently riskier approach).

In China the results of the corporate payment behaviour survey paint a very different picture. 4% of B2B invoices were written off last year and 46% were paid late. Although the write-off rate in China was half the amount reported in the US, it has increased by 33% compared to the survey we did in 2019, before the global pandemic hit. To protect their own cash flow, businesses in Vietnam should monitor the ongoing creditworthiness of their individual customers in addition to noting trends in each market’s payment practices.

A key reason behind such contrasting payment behaviours is the different experience of the Covid-19 pandemic faced by businesses in each market. China has been relatively successful in containing the pandemic and as a result has experienced less domestic business disruption. In addition, China has benefited from some pent-up export demand caused by international supply chains disruptions.

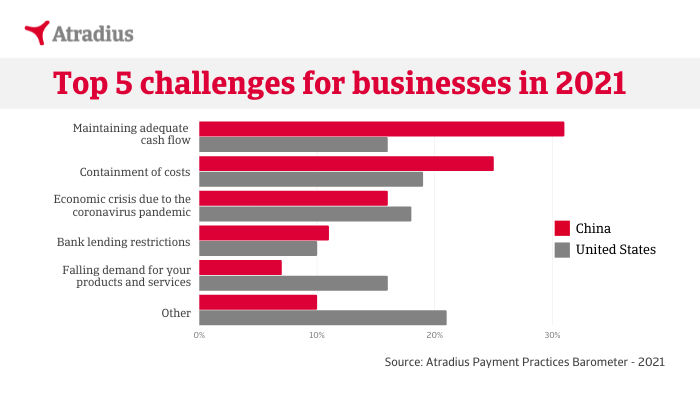

Looking ahead, both of Vietnam’s major markets have expressed optimism. 60% of US businesses and 55% of businesses in China anticipate the trading environment to improve over the next 12 months. Despite the optimism, maintaining adequate cash flow and containing costs under the current difficult global economic situation are cited as the top greatest challenges for these businesses. To navigate through this uncertain period, companies should adopt a holistic and flexible credit management approach to mitigate risk associated with trades with domestic and overseas buyers.

How to minimise credit risk

When seeking to minimise credit risk, the golden rule for every business offering trade credit is know your customer. If your customer is experiencing financial distress, they may take longer to pay your bill, or even default on the payment entirely. Resources such as the Atradius Payments Practices Barometer Survey can be useful in providing a snapshot of a market and its local sectors. Although they will not be able to pinpoint the fiscal health of your individual customer, they can act as a useful warning and provide you with insight into the local situation. For example, this year’s US Survey shows that the steel/metals industry is facing many challenges with high percentages of late payments and write-offs, and a third of businesses reporting a deterioration in their customers’ payment practices. As a result, businesses in Vietnam may benefit from taking additional steps to protect their accounts receivable when trading with the US steel / metals industry.

Key steps for strong credit management

Active management of your credit accounts is critical to a successful credit management policy. This involves the ongoing monitoring of your customers’ financial situation, as well as the financial health of your customers’ sectors and markets. The global recession sparked by the Covid-19 pandemic, in particular, has led to widespread economic stress and is a key reason why extra vigilance is required.

A trade credit insurance company such as Atradius that operates in international markets will have information on sector performance trends and credit risk profile of more than 250 million businesses around the world. Such data can be invaluable in helping you assess the creditworthiness of both prospects and customers and will help you determine whether to offer trade credit and, if so, how much and what payment terms you wish to apply.

Making the most from international trade

The safest way to protect your accounts receivable from the risk of bad debts and late payments is to demand cash up front for all of your sales. However, in a competitive international market, failure to support the liquidity of your customers with trade credit and favourable payment terms may mean the difference between winning and losing key contracts and may impact business growth.

With trade credit insurance your business can trade with confidence, with the knowledge that your invoices will be paid even if your customer goes bust. What’s more, you can leverage the business intelligence and underwriter knowledge of your credit insurance company to help you identify which businesses and markets represent the greatest risks and where you might find opportunities for growth.

For businesses in Vietnam exploring the significant opportunities for growth presented by international trade, a strategic approach to credit management grounded in high quality business intelligence could be the key difference between business success and failure.

By Hanh Vu, Country Manager, Atradius Information Services Vietnam Co. Ltd.

About the author: Hanh Vu has extensive experience helping businesses identify domestic and export trade opportunities through active management of credit or trade receivable risks. With more than 15 years of experience in accounting, economic research and business development, Hanh currently head up Atradius business in Vietnam.Atradius is a global provider of credit insurance, bond and surety, collections and information services, with a strategic presence in over 50 countries. In Vietnam, Atradius works with our official local partners to provide customers with timely information about trade credit risks on companies in Vietnam.To learn more: https://atradius.sg.For enquiry: info.vn@atradius.comFollow us on LinkedIn: https://www.linkedin.com/company/atradiusasiaTo learn more about what is trade credit insurance, visit this page: https://baohiemtindungthuongmailagi.vn/